Royal Caribbean Travel Insurance - 2026 Review

Royal Caribbean Travel Insurance - Review

7

Strengths

- Strong Insurance Partner

- Available at Check-Out

Weaknesses

- Weak Medical Cover

- Weak Evacuation Cover

- No Pre-Existing Medical Waiver

Sharing is caring!

Despite what the name would imply, Royal Caribbean doesn’t only sail in the Caribbean. This premiere cruise line will take you across the seas to dream destinations from Alaska to the Amalfi Coast. With so many places to explore far from home, Royal Caribbean understands the importance of travel insurance. That is why they offer their own travel insurance package whenever a customer books a cruise with Royal Caribbean.

Sample Cruise Itinerary

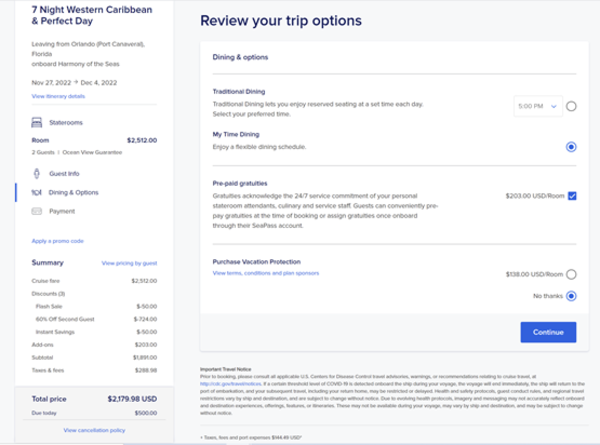

For comparison purposes, we chose the example of a Royal Caribbean 7-Night Western Caribbean & Perfect Day cruise that begins and ends in Orlando, Florida. Cruise dates chosen were 11/27/2022 – 12/4/2022. Travelers are two adults aged 59. The cruise price is $2,179.98.

As airfare is purchased separately and pricing can greatly vary, this review includes only the cost of the cruise, instead of total trip cost including airfare.

Royal Caribbean only offers one comprehensive policy, and it’s a simple “check yes or no” situation as you’re selecting your additional options on their website before checking out.

Our $2,179.98 cruise has an insurance cost of $138 if bought through Royal Caribbean. The plan offered is called the Royal Caribbean Travel Protection Program, and it provides the following coverage:

- $25k Emergency Travel Medical Insurance

- $50k Emergency Medical Evacuation Insurance

- 90% refund of cruise credits if you Cancel for Any Reason

In our opinion, this medical coverage is generally not enough for someone who is travelling internationally. To understand it another way, this would be like insuring your car to the state minimum required limits. It’s enough to get you on the road, but will it be enough if you need to use it? In our experience, it is not.

Moreover, we have an issue with the Cancel For Any Reason benefit that is offered. We feel that if you cancel, you should get your money back. What if you decide you don’t want to cruise after all? To us, a refund of cruise credit is not a true refund. We recommend a policy that gives you cash back — a true refund — if you cancel your trip.

Comparison Quotes

Based on our sample couple, ages 59 and 59, we created comparison quotes using TripProtectors’s travel insurance marketplace engine. The trip cost used for the comparison is the cruise cost for both travelers of $2179.

When traveling outside the United States, we recommend a minimum coverage of $100,000 in Medical Insurance, $250,000 in Medical Evacuation, and a Pre-existing Medical Condition Waiver. We used these criteria to choose the selected quotes. Since the Royal Caribbean Travel Protection Program includes their Cancel For Any Reason benefit as standard, we compared their policy to our Cancel For Any Reason (CFAR) plans.

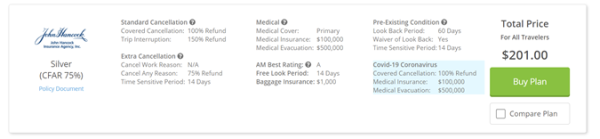

The least expensive Cancel For Any Reason plan with adequate coverage on our quote from TripProtectors is the John Hancock Silver (CFAR 75%).

Next, we broke down the benefits of each policy in a side-by-side comparison.

|

Benefit |

Royal Caribbean Travel Protection Program |

John Hancock Silver (CFAR 75%) |

|

Trip Cancellation |

100% of trip cost |

100% of trip cost |

|

Trip Interruption |

150% of tip cost |

150% of trip cost |

|

Medical Insurance |

$25,000 |

$100,000 |

|

Medical Evacuation |

$50,000 |

$500,000 |

|

Baggage Loss/Damage |

$1,500 per person |

$1,000 per person |

|

Baggage Delay |

$500 |

$500 |

|

Travel Delay (Incl quarantine) |

$500 |

$750 ($150/day) |

|

Missed Connection |

$300 |

$750 per person |

|

Cover Pre-existing Medical Conditions |

No |

Yes if purchased within 14 days of deposit |

|

Cancel For Work Reason |

No |

No |

|

Interrupt For Any Reason |

No |

No |

|

Cancel For Any Reason

|

90% in Cruise Credits |

75% of trip cost |

|

Accidental Death & Dismemberment |

No |

$100,000 |

|

Cost of Policy |

$138 (6% of Trip Cost) |

$201 (9% of Trip Cost) |

Cost Comparison

Overall, the Royal Caribbean Travel Protection Program has minimal coverage. Their CFAR benefit only provides a cruise credit valid for one year.

By shopping for cruise insurance through TripProtectors our two travelers can have 4 times the Medical Insurance, double their Emergency Medical Evacuation insurance, and receive actual cash back if they choose to cancel for a reason not specified in the policy. We feel it’s important for travelers to know that a policy with more appropriate coverage limits is available for only $31.50 more per person.

In the following sections, we discuss know what to look for when shopping for travel insurance for your Royal Caribbean cruise.

Trip Cancellation

A significant concern for travelers is Trip Cancellation. If you became ill or had an accidental injury prior to your departure date, you may have to cancel your travel arrangements, resulting in financial losses. While disappointing, Trip Cancellation is doubly painful without cancellation insurance.

Royal Caribbean Travel Protection Program permits cancellation for the following reasons:

- Unexpected injury, illness, or death of traveler or family member.

- Involvement of a traffic accident that causes you to miss your cruise

- Residence uninhabitable by natural disaster, fire, flood, burglary

- Revocation of military leave

- Subpoena or being called to serve jury duty

Unfortunately, Royal Caribbean’s list of cancellation reasons lacks some important coverages.

We recommend policies that also include:

- Strikes

- Terrorism

- Default or bankruptcy of the common carrier or travel supplier

- Cancel For Work Reason (traveler required to work during the trip)

- Employer-initiated transfer of 250 miles or more

- Destination uninhabitable or unreachable by fire, flood or natural disaster

- Mechanical breakdown of a common carrier

- Mandatory evacuation

- Hurricanes

- Inclement weather

- Documented theft of passports or visas.

The Royal Caribbean Travel Protection Program also does not cover any travel arrangements booked outside Royal Caribbean.

The John Hancock Silver (CFAR 75%) policy can cover all travel arrangements, regardless of where you booked them. In addition, this plan offers a broad list of covered reasons, including cancelling due to contracting COVID.

Trip Interruption

A Trip Interruption is a situation during your trip that causes you to miss some or the rest of your vacation. It’s like Trip Cancellation but happens during your travels.

The most common trip interruption is the injury or illness of a traveler. If you had an injury or illness on your vacation but can continue traveling after treatment, trip interruption reimburses the unused portion of the trip, and the cost to rejoin the trip in progress.

Trip interruption also includes a family member who had a sudden grave illness or passed away. If your covered situation requires curtailing the trip and going home early, Trip Interruption also reimburses for the unused portion of the trip, plus the added cost of going home early.

In the Royal Caribbean Travel Protection Program, Trip Interruption benefits share the same short list of covered reasons as Trip Cancellation.

Cancel For Any Reason

Cancel For Any Reason cruise insurance provides the highest level of flexibility and reimbursement if you must cancel your trip for any reason not covered by the policy.

If you cancel your Royal Caribbean cruise for a reason not listed in their travel policy, they grant future credits for 90% of the prepaid, non-refundable cancellation fees paid to them. Credits expire after one year, are non-transferrable and not redeemable for cash. Royal Caribbean, not their insurance policy, provides this part of the Travel Protection Program. When it comes to refunds, we always prefer cash since future credits may not be used.

Alternatively, travel insurance policies like John Hancock Silver (CFAR 75%) pay a 75% cash refund of all prepaid, non-refundable trip costs including arrangements made outside of Royal Caribbean. This could include flights, hotels, rental cars, excursions and transfers.

Cancel For Any Reason policies have several stipulations:

- Purchase the policy within 10 - 21 days (depending on policy), of your initial payment or deposit date and

- Insure 100% of the prepaid trip costs subject to cancellation penalties or restrictions. For additional prepaid non-refundable payments made after the purchase of the policy, insure within 10-21 days (depending on policy), of each subsequent payment added to your trip, and

- Cancel your trip 2 days or more before your scheduled departure date.

Medical Insurance for Emergency Treatment

One of the most important factors in selecting trip insurance is having adequate Medical Insurance when you travel. Anything can happen, including accidental injuries or sudden illness.

If you have a medical emergency when traveling and don’t have proper medical insurance coverage while overseas, you could find yourself with huge, unexpected hospital bills. Many Americans mistakenly believe countries with universal health care will treat them for free. Unfortunately, this is not the case.

Instead, Americans receive treatment at private hospitals, not public, and must pay like anyone else. Admission for inpatient care can cost $3,000-$4,000 per day, plus the cost of treatment, x-rays, surgeries, and specialists.

A common misconception is that Medicare will pay for hospitalization overseas. Unfortunately, they won’t. Medicare does not pay providers outside the US. Some Medicare supplements do cover overseas, but have lifetime limits or reduced benefits, and pay for emergencies only. They can still require you to pay 20% of the costs. As a result, you could go on vacation and end up with medical bills in the thousands.

TripProtectors urges overseas travelers to take travel medical insurance of at least $100,000 per person. In a medical emergency, $100,000 provides ample health care and helps protect your retirement savings from unexpected financial burdens.

Royal Caribbean provides a $25,000 benefit for Medical Insurance. John Hancock’s Silver (CFAR 75%) policy includes $100,000 per person of Medical Insurance, so you can receive proper treatment without ending up in debt.

Emergency Medical Evacuation

Medical Insurance isn’t the only potentially expensive part of a trip. Emergency Medical Evacuation transports you from the place of injury or illness to the closest hospital. Once you’re stable enough for transport, Medical Evacuation brings you home via commercial flight or, if necessary, private medical jet.

Medical flights can cost up to $25,000 per hour and regular health insurance does not cover it. In addition, the US State Department does not offer any medical treatment or evacuation assistance for US citizens. TripProtectors advises travelers to get at least $250,000 Medical Evacuation to assure there’s enough coverage to get them back home from almost anywhere if they experience a serious medical event. However, if traveling to Asia or Africa or beyond, we recommend a minimum of $500,000 for Emergency Medical Evacuation due to the distance from the US.

The Royal Caribbean Travel Protection Program includes Medical Evacuation up to $50,000 per person.The John Hancock Silver (CFAR 75%) offers $500,000 per person for Medical Evacuation, so you can feel secure knowing you have adequate coverage to transport you back home if needed.

Pre-existing Medical Conditions

A significant concern for senior travelers can be pre-existing medical conditions. A Pre-Existing Medical Condition is one in which you’ve received medical treatment, testing, medication changes, added new medications, or received a recommendation for a treatment or test that hasn’t happened yet. Most travel insurance policies exclude pre-existing conditions unless you purchase the policy within the required time period from your initial trip deposit date (called the Time Sensitive Period). Otherwise, the insurer will look backward 60, 90, or 180 days (depending on the policy) from the date you purchased the insurance to see if there are any pre-existing medical conditions they won’t cover. This is called the Look Back Period. Any medical conditions older than this Look Back Period, unchanged or stabilized with no medication dosage changes are covered, as are any new conditions that arise after you purchase the policy.

If you must cancel, interrupt, or seek medical treatment for a medical condition while traveling, travel insurance policies typically exclude claims related to Pre-existing Medical Conditions. However, if you purchase the policy within a few days of your Initial Trip Payment or Deposit date, many policies add a Waiver to the policy that covers Pre-existing Conditions. As a result, there is no Look Back Period and Pre-existing Conditions are covered.

The Royal Caribbean Travel Protection Program does not cover Pre-Existing Conditions inside the Look Back Period of 60 days.

The John Hancock Silver (CFAR 75%) covers Pre-existing Medical Conditions if you purchase within the 14-day Time Sensitive Period.

Price and Value

The Royal Caribbean Travel Protection Program offers minimal coverage for a relatively similar price as other available options. The medical insurance coverage is only $25,000, and only $50,000 medical evacuation, which may not be adequate for a serious illness or injury. It does not offer a Pre-Existing Condition Exclusion Waiver. Cancellation reasons are limited, and the Cancel For Any Reason option only grants future cruise credits that expire after a year. Overall, the Royal Caribbean Travel Protection Program offers limited value for the price.

In contrast, by comparison shopping, we found the John Hancock Silver (CFAR 75%) policy comes in at $201 (only $63 more than the Royal Caribbean plan!) It includes superior medical and evacuation benefits, a pre-existing medical condition waiver if purchased within a Time Sensitive Period of 14 days from the deposit date, and a robust list of cancellation reasons. Plus, it includes a Cancel For Any Reason provision that refunds 75% of trip costs back in cash, rather than future credit. It has superior coverage over Royal Caribbean’s policy at minimal additional cost.

Conclusion

Royal Caribbean Travel Protection Program cruise insurance provides travelers with a minimal insurance policy and could leave travelers unpleasantly surprised during an emergency. Medical coverage and medical evacuation limits are low, and there are a limited number of covered cancellation and interruption reasons. Overall, we rate it a 7 out of 10.

Travelers planning a Royal Caribbean cruise vacation will find the best value for their money and peace of mind when they shop for travel insurance at TripProtectors Travel Insurance Marketplace. There, you can review dozens of options and select the best policy to fit your needs.

To help you find the best policy, TripProtectors recommends having at least $100,000 in travel medical coverage and $250,000 emergency medical evacuation when traveling outside the US. And, if you purchase the policy within the 14-21 days of initial trip payment, please consider a travel insurance policy with the pre-existing condition waiver included to ensure the most coverage for your money.

If you are planning a Royal Caribbean cruise in 2022, be sure to pack insurance before you travel. You never know when you may need it.

Have questions? Chat with us online, send us an email at agent@TripProtectors.com or alternatively call us at +1(650) 397-6592. We would love to hear from you.

Safe Travels!

This article has been written for review purposes only and does not suggest sponsorship or endorsement of AARDY by the trademark owner.

Recent AARDY Travel Insurance Customer Reviews

Donna M.

Good coverage for a fair price!

Good coverage for a fair price!

Rita Swensoncustomer

The agent was very friendly

The agent was very friendly, informative, and patient with all my questions.

customer Wayne

This is the fourth time we have used…

This is the fourth time we have used Aardy for our travel insurance.Excellent customer service.our friends we travel with use Aardy as well.I would recommend them to our family and friends.